As Indonesia’s largest commerce businesses approach IPO scale and considering the dominance of Shopee, Tokopedia, Bukalapak, and Lazada, there can be few opportunities left in the e-commerce space.

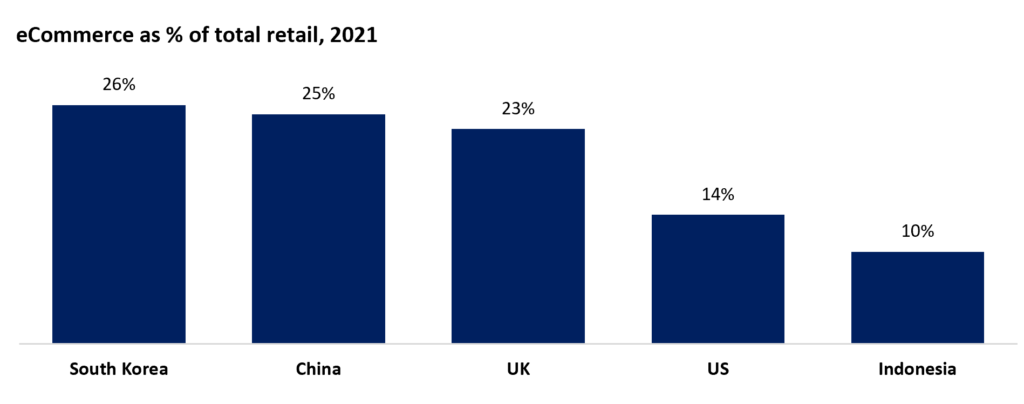

However, even as the pandemic shifts online purchase behaviour to overdrive, our estimates put total e-commerce as a percentage of retail sales in Indonesia at just over 10 per cent.

Compared to more developed markets like China, with ~25 per cent e-commerce penetration, there is still room for multiples times of growth.

Source: UNCTAD

The onset of the COVID-19 pandemic accelerated new users into the digital economy in e-commerce and major sectors such as logistics, education, and fintech, all of which experienced significant increases in adoption rates.

However, even though e-commerce is the most mature sector overall, there are still blue ocean verticals to be found.

Underlining this growth is not only greater adoption by existing users but, most significantly, new users.

Based on data from Google, Temasek, and Bain & Company studies, one in three of all digital service consumers in 2020 were new users resulting from the impact of COVID-19, and survey data suggest that these new users will continue to retain new online habits past the pandemic.

Additionally, the majority of these new users were from non-metro areas. But where do the following e-commerce opportunities lie? This requires a deeper look at the different penetration rates of online purchase behaviour per sector, revealing the following key observations.

Also Read: Rakuten empowering SMEs to online shopping in Indonesia

Uncovering frontier customers and product categories

The most straightforward way to think about e-commerce opportunities is to think of frontier customers and frontier product categories. A basic illustration shows where opportunities are emerging:

Source: Euromonitor (2020), AC Ventures analysis

Frontier customers in the e-commerce space include consumers in tier 2-4 cities and enterprises with more complex purchase requirements ranging from MSMEs to larger corporations with different vendor arrangement policies.

Based on the latest estimates, only 57 per cent of Indonesia’s population live in urbanised areas suggesting easily over 100M consumers living in rural and village communities.

This represents an enormous opportunity as online commerce penetration within rural Indonesia is far less than in urbanised areas.

Separately, MSMEs, which we have written about previously, are also frontier eCommerce customers as they are usually slow in the adoption of digital technology.

In this customer segment, over 63 million MSMEs represent over 60 per cent of Indonesia’s GDP and 97 per cent of the total workforce; there are enormous opportunities to be unlocked by adopting e-commerce for B2B e-commerce supplies for this sector.

Source: The Finery Report (2020)

Frontier products represent another highly attractive opportunity. Historically around the world, penetration rates of different product categories going online have differed considerably.

It’s well known that Amazon started with books before moving onto electronics, various household items, and only more recently, groceries.

Similarly, we can see that while Indonesia’s horizontal marketplaces have a considerable selection of electronics and household items, there’s far less selection in groceries, and even then, the product experience is not ideal. Beyond the physical product itself, we must also consider the product experience.

For example, when consumers shop for groceries, they expect to receive items on the same day.

Hence, we also need to consider the product and the product experience – which requires fundamentally differentiated logistics last mile and supply chains compared to selling electronics.

Drivers for emerging opportunities

There are several drivers for these emerging opportunities. Firstly – the consumers. Accelerated by lockdowns imposed by governments and hesitancy to visit crowded markets, more and more consumers have tried purchasing new product categories online, such as groceries.

Several purchases later, what initially felt foreign becomes a habit, so we’ve seen incredible growth rates in this sector. Having backed early entrants to this space, such as Segari, we are witnessing this growth first hand.

Also Read: How millennials and the pandemic are driving the growth of cloud kitchens in Indonesia

Another driver is the vastly improved infrastructure supporting e-commerce.

From logistics to payments to internet penetration rates, improvements to these key supporting areas have increased the reach and penetration of e-commerce such that increasingly hard-to-reach areas have become viable markets for e-commerce.

Emerging models addressing frontier customers and products

The maturing consumer and infrastructure open up these opportunities and differentiated models that help create better access to new customers and the delivery of new product verticals.

These new models also provide a competitive advantage to new startups compared to incumbent platforms addressing these sectors.

For example, the PinDuoDuo (PDD) model pioneered online social commerce via group buying. Group buying initially found its strongest appeal with emerging consumers attracted by low prices (enabled by bulk buying) and buying with friends, which helped bridge a trust gap of buying online.

The model has evolved since then, but the entry point was highly differentiated compared to the marketplace incumbents of Taobao and JD at the time.

Similarly, we see several social commerce models in Indonesia employing various forms to address new customers through group purchases and lower prices.

Companies such as Kitabeli and Rumahan use the mechanics of group purchases in 2nd and 3rd tier cities to enable emerging consumers to buy online.

The former focuses on more daily use items while the latter use installed payments via community financing to purchase higher average order value goods like household appliances.

Other types of differentiated models can help with enabling improved product experiences. For example, another model that emerged from China helped accelerate online purchases for fresh produce.

Known as Community Group Buy (“CGB”), this model leverages neighbourhood “agents” in the community who help solve for customer acquisition and last-mile delivery logistics.

This particular model bridges user trust gaps and addresses logistic bottlenecks as shipping small baskets of daily groceries can become prohibitively expensive at the last mile.

Also Read: The road to success for e-commerce players in Indonesia is paved with data and talent acquisition

In this model, the agent aggregates the entire community’s purchase orders and takes on the responsibility for delivering within the catchment area. Our portfolio company Segari which we backed in 2020 at the pandemic, has also executed this model to great success.

Another “new customer segment” worth noting is the increasing adoption of e-commerce platforms by MSMEs in Indonesia.

Historically warung owners would have to close their stores to shop – sometimes several times a day – and pick up inventory to sell. Clearly, this is a massive inefficiency for the store as wholesalers could sometimes take several hours round trip.

By bringing the convenience of ordering supplies online and saving from shortening the supply chain, companies such as Ula are empowering MSMEs with efficiency and savings that can be put back into growing their businesses. Still, other businesses can support small enterprises to sell online a “Shopify for offline businesses” such as Majoo.

There are also plenty more emerging models, including “dark” convenience stores, cloud kitchens, and the vast category of direct-to-consumer brands, all of which are chipping away at the multi-hundred billion dollars offline retail market share more and more consumers spend time and money online.

Indonesia’s total retail market is on track to cross US$300 billion in the next three years, and with e-commerce just reaching US$30 billion in 2020, there are still excellent growth prospects.

For example, the largest single share of groceries alone makes up over US$70 billion, with estimates of online penetration barely crossing 0.5 per cent in 2021.

At AC Ventures (ACV), our view is that e-commerce penetration will cross 30 per cent in the next five years, creating over US$60 billion in market value opportunities and multiple startup investment opportunities.

Hence there has never been a better time backing Indonesia’s next generation of entrepreneurs, even in a seemingly mature space such as e-commerce.

–

Editor’s note: e27 aims to foster thought leadership by publishing views from the community. Share your opinion by submitting an article, video, podcast, or infographic

Join our e27 Telegram group, FB community, or like the e27 Facebook page

Image credit: Ula

The post Capturing the next frontier opportunities in the Indonesian e-commerce landscape appeared first on e27.

This maximized goal muscle fiber recruitment and considerably lowered the risk

of harm. Do you know what’s the primary factor that will prevent you from building huge

shoulder muscles? The shoulders may be probably the most underappreciated muscle group within the higher physique.

However, well-defined shoulders improve your

physique as much as any other muscle.

This isn’t all flash; it’s a novel urgent problem because

of the longer levers than traditional implements.

After the lateral raise, the front raise must be a simple idea.

By shifting your place, you may shift the main target

to your front delts as a substitute.

This magnificence builds strength and endurance in your front delts

and fires up your core for some actual strong stability work.

It’s a fantastic thought to begin a exercise with a compound

train the place you possibly can transfer

as much weight as attainable. In a chest, shoulder, and tricep workout, that may be the flat bench press.

As a bodybuilder, energy isn’t the end-all-be-all, however

progressive overload is still a fundamental precept for muscle

growth. Cable lateral raises provide constant pressure on the lateral deltoids all through the full

range of movement, making them a priceless addition to your

shoulder workouts. You can do these with the cable attachment at

the backside or just below your waist. Cable exercises are an effective way to

help hold fixed pressure on the muscle.

In reality, the Farmer’s Carry is a superb exercise

to include in every dumbbell exercise session. You can follow the workout calendar below

for a complete 4 weeks of full body coaching with day by

day exercise routines. The mixture of these 7 parts won’t solely hit all the most important functions of human efficiency, but will lend itself to choosing the right workouts for constructing muscle.

Not only will I present you the workouts, I’ll explain why

I selected every single train for this full-body health club workout routine.

It’s very onerous to make use of heavy weight with correct kind on face pulls

as it typically causes you to just tip over or use different

muscles as an alternative. But for the seated variations, we

were actually able to use slightly heavier

weights than the standing variations due to the additional

stability provided by the bench. Probably as a end result of this,

for all three of us — though not by a lot — the seated versions carried out the best.

I do suggest that you start out with some kind of free weight

urgent exercise for shoulders. You’ll form, build, and chisel those muscular tissues with the remaining superset exercises.

It entails driving your elbows in instead of taking your arms out.

With the mix of reverse fly, the cable face pull helps construct

robust posterior delts and wholesome shoulders.

Together, these three segments of the deltoid contribute to

a variety of arm movements, together with lifting, rotating,

and abducting the arms. Robust and well-developed deltoids enhance the aesthetic attraction of the shoulders and

contribute to overall shoulder perform and stability.

I sit at a desk a lot of the day, so I get an enormous bang for my buck with these.

However keep in mind that the front delt already gets enough indirect work by way of a number of pressing movements.

In addition, keep away from utilizing momentum to raise the weights,

as doing so decreases the effectiveness of the exercise. Let the supposed

muscular tissues do all the work, and you’ll be rewarded

with larger features. For the second exercise, we’re

moving away from the barbell with the incline dumbbell press, top-of-the-line chest workout routines emphasizing your upper pecs.

You would possibly need 20 or extra sets per week if

you are a sophisticated bodybuilder or lifter.

In that case, you possibly can improve your workout frequency

(and your gains) to twice weekly.

With the help of our programming ideas and killer shoulder workout,

you’ve got obtained everything you should build the boulder shoulders of your dreams.

In truth, we would go so far as to say that one of the primary objectives of most bodybuilders is

to construct large delts, as it plays a huge

function in total aesthetics. The barbell rear delt row works the

again of your shoulder and mid trapezius.

References:

Arnold schwarzenegger Steroid regimen