Managed care plays a major role in the delivery of health care to Medicaid enrollees. With 69% of Medicaid beneficiaries enrolled in comprehensive managed care plans nationally, plans have played a key role in responding to the COVID-19 pandemic and in the fiscal implications for states. This brief describes 10 themes related to the use of comprehensive, risk-based managed care in the Medicaid program and highlights significant data and trends. Understanding these trends provides important context for the role managed care organizations (MCOs) play in the Medicaid program overall as well as during the ongoing COVID-19 public health emergency (PHE) and in its expected unwinding. CMS released guidance for state Medicaid agencies outlining how managed care plans can promote continuity of coverage for individuals as states resume normal operations when the continuous coverage requirement during the public health emergency ends. While we can track state requirements for Medicaid managed care plans, plans have flexibility in certain areas including in setting provider payment rates and plans may also choose to offer services beyond those required in the Medicaid state plan or waivers. States also make decisions about which populations and services to include in managed care arrangements leading to considerable variation across states.

1. Today, capitated managed care is the dominant way in which states deliver services to Medicaid enrollees.

States design and administer their own Medicaid programs within federal rules. States determine how they will deliver and pay for care for Medicaid beneficiaries. Nearly all states have some form of managed care in place – comprehensive risk-based managed care and/or primary care case management (PCCM) programs., As of July 2021, 41 states (including DC) contract with comprehensive, risk-based managed care plans to provide care to at least some of their Medicaid beneficiaries (Figure 1). North Carolina is the latest state to be included in this count, having launched comprehensive risk-based Medicaid managed care statewide on July 1, 2021. Medicaid MCOs (also referred to as “managed care plans”) provide comprehensive acute care and in some cases long-term services and supports to Medicaid beneficiaries. MCOs accept a set per member per month payment for these services and are at financial risk for the Medicaid services specified in their contracts. States have pursued risk-based contracting with managed care plans for different purposes, seeking to increase budget predictability, constrain Medicaid spending, improve access to care and value, and meet other objectives. While the shift to MCOs has increased budget predictability for states, the evidence about the impact of managed care on access to care and costs is both limited and mixed.,

2. Each year, states develop MCO capitation rates that must be actuarially sound and may include risk mitigation strategies.

States pay Medicaid managed care organizations a set per member per month payment for the Medicaid services specified in their contracts. Under federal law, payments to Medicaid MCOs must be actuarially sound. Actuarial soundness means that “the capitation rates are projected to provide for all reasonable, appropriate, and attainable costs that are required under the terms of the contract and for the operation of the managed care plan for the time period and the population covered under the terms of the contract.” Unlike fee-for-service (FFS), capitation provides upfront fixed payments to plans for expected utilization of covered services, administrative costs, and profit. Plan rates are usually set for a 12-month rating period (which typically run on a calendar year or state fiscal year basis) and must be reviewed and approved by CMS each year. States may use a variety of mechanisms to adjust plan risk, incentivize plan performance, and ensure payments are not too high or too low, including risk sharing arrangements, risk and acuity adjustments, medical loss ratios (MLRs, which reflect the proportion of total capitation payments received by an MCO spent on clinical services and quality improvement), or incentive and withhold arrangements.

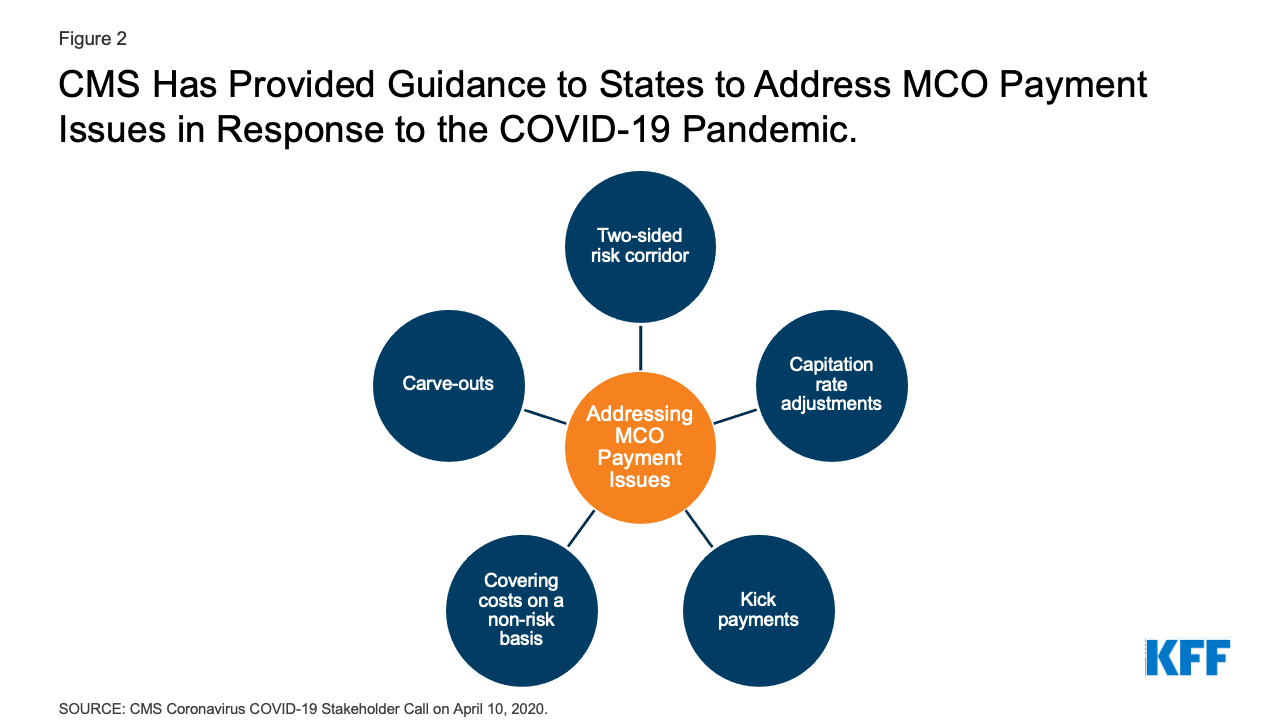

CMS allowed states to modify managed care contracts in response to unanticipated COVID-19 costs and conditions that led to decreased utilization. States have several options to address these payment issues including risk mitigation strategies, adjusting capitation rates, covering COVID-19 costs on a non-risk basis, and carving out costs related to COVID-19 from MCO contracts (Figure 2). These options vary widely in terms of implementation/operational complexity, and all options require CMS approval. More than half of MCO states reported implementing COVID-19-related risk corridors in their 2020 or 2021 contracts. Of these states, about half reported that they have or will recoup funds, while recoupment for the remaining states was undetermined at the time of KFF’s annual 50-state Medicaid budget survey. Analysis of National Association of Insurance Commissioners (NAIC) data for the Medicaid managed care market show that annual loss ratios in 2020 (in aggregate across plans) decreased by four percentage points from 2019 (and three percentage points from 2018), but still met the 85% minimum even without accounting for potential adjustments. As 2022 begins, states and plans face continued uncertainty related to the pandemic’s trajectory which may continue to impact utilization patterns and result in rate setting challenges for states.

Figure 2: CMS Has Provided Guidance to States to Address MCO Payment Issues in Response to the COVID-19 Pandemic.

3. As of July 2019, more than two-thirds (69%) of all Medicaid beneficiaries received their care through comprehensive risk-based MCOs.

As of July 2019, 53.7 million Medicaid enrollees received their care through risk-based MCOs. Twenty-five MCO states covered more than 75% of Medicaid beneficiaries in MCOs (Figure 3).

Although 2019 data (displayed above) are the most current national data available on Medicaid MCO enrollment, enrollment in Medicaid overall has grown substantially since the start of the coronavirus pandemic in February 2020. This enrollment growth reflects both changes in the economy as well as provisions in the Families First Coronavirus Response Act (FFCRA) that require states to ensure continuous coverage for current Medicaid enrollees to access a temporary increase in the Medicaid match rate during the PHE period. KFF analysis of more recent MCO enrollment data, from the subset of states that make these data available, shows growth in Medicaid MCO enrollment during the pandemic tracks overall Medicaid enrollment trends. When the continuous coverage requirements end, states will begin processing redeterminations and renewals and millions of people could lose Medicaid coverage if they are no longer eligible or face administrative barriers during the process despite remaining eligible. CMS has released guidance and strategies for states to help maintain coverage of eligible individuals after the end of continuous enrollment requirements, including guidance outlining how managed care plans can support states in promoting continuity of coverage.

4. Children and adults are more likely to be enrolled in MCOs than seniors or persons with disabilities; however, states are increasingly including beneficiaries with complex needs in MCOs.

As of July 2021, 37 MCO states reported covering 75% or more of all children through MCOs (Figure 4). Of the 38 states that had implemented the ACA Medicaid expansion as of July 2021, 31 states were using MCOs to cover newly eligible adults and the large majority of these states covered more than 75% of beneficiaries in this group through MCOs. Thirty-four MCO states reported covering 75% or more of low-income adults in pre-ACA expansion groups (e.g., parents, pregnant women) through MCOs. In contrast, only 19 MCO states reported coverage of 75% or more of seniors and people with disabilities. Although this group is still less likely to be enrolled in MCOs than children and adults, over time, states have been moving to include seniors and people with disabilities in MCOs.

5. In recent years, many states have moved to carve in behavioral health services, pharmacy benefits, and long-term services and supports to MCO contracts.

Although MCOs provide comprehensive services to beneficiaries, states may carve specific services out of MCO contracts to fee-for-service (FFS) systems or limited benefit plans. Services frequently carved out include behavioral health, pharmacy, dental, and long-term services and supports (LTSS). However, there has been significant movement across states to carve these services in to MCO contracts. While the vast majority of states that contract with MCOs report that the pharmacy benefit is carved in to managed care (35 of 41), five states report that pharmacy benefits are carved out of MCO contracts as of July 2021 (Figure 5). Three states report plans to carve out pharmacy from MCO contracts in FY 2022 or later (California, New York, and Ohio).

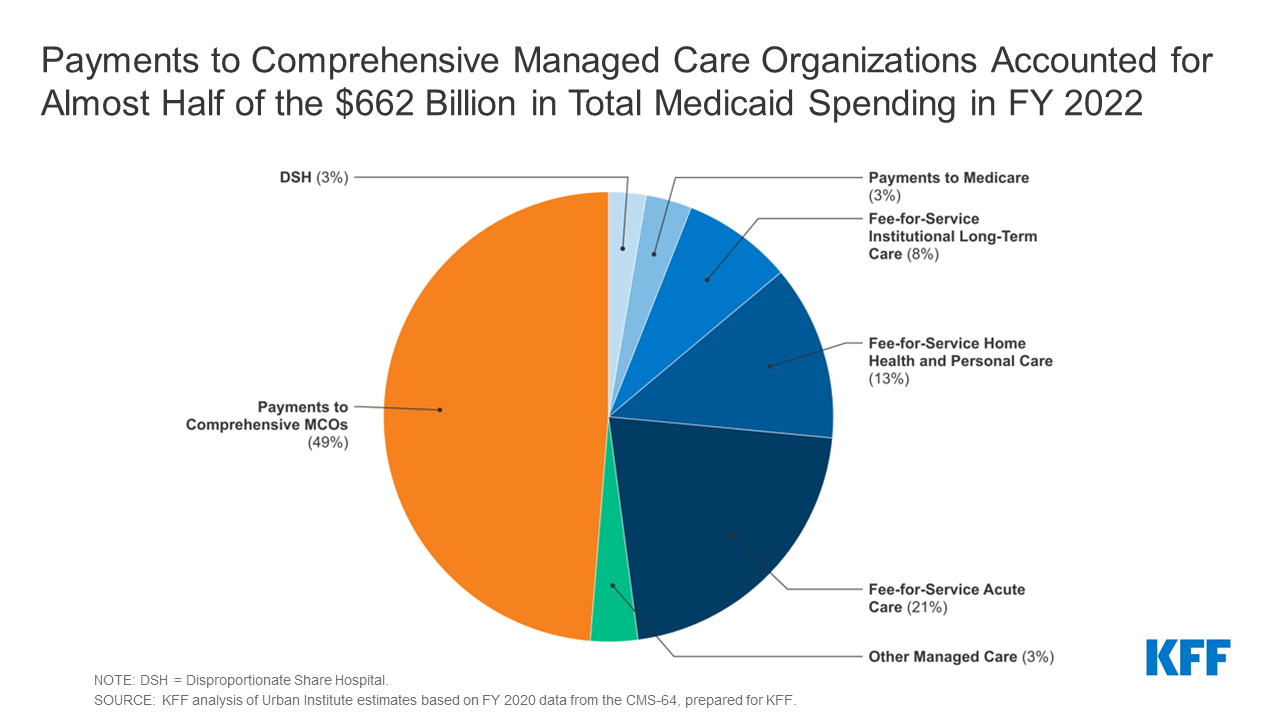

6. In FY 2020, payments to comprehensive risk-based MCOs accounted for the largest share of Medicaid spending.

In FY 2020, state and federal spending on Medicaid services totaled over $662 billion. Payments made to MCOs accounted for about 49% of total Medicaid spending (Figure 6), an increase of almost three percentage points from the previous fiscal year. The share of Medicaid spending on MCOs varies by state, but over three-quarters of MCO states directed at least 40% of total Medicaid dollars to payments to MCOs (Figure 7). The MCO share of spending ranged from a low of about 2% in Colorado to 88% in Kansas. State-to-state variation reflects many factors, including the proportion of the state Medicaid population enrolled in MCOs, the health profile of the Medicaid population, whether high-risk/high-cost beneficiaries (e.g., persons with disabilities, dual eligible beneficiaries) are included in or excluded from MCO enrollment, and whether or not long-term services and supports are included in MCO contracts. As states expand Medicaid managed care to include higher-need, higher-cost beneficiaries, expensive long-term services and supports, and adults newly eligible for Medicaid under the ACA, the share of Medicaid dollars going to MCOs will continue to increase.

7. A number of large health insurance companies have a significant stake in the Medicaid managed care market.

States contracted with a total of 282 Medicaid MCOs as of July 2019. MCOs represent a mix of private for-profit, private non-profit, and government plans. As of July 2019, a total of 16 firms operated Medicaid MCOs in two or more states (called “parent” firms), and these firms accounted for 63% of enrollment in 2019 (Figure 9). Of the 16 parent firms, seven are publicly traded, for-profit firms while the remaining nine are non-profit companies. Six firms – UnitedHealth Group, Centene, Anthem, Molina, Aetna/CVS, and WellCare – each have MCOs in 12 or more states (Figure 8) and accounted for 51% of all Medicaid MCO enrollment (Figure 9). All six are publicly traded companies ranked in the Fortune 500. KFF analysis of more recent MCO enrollment data, from the subset of states that make these data available, showed that five for-profit parent firms (Centene, Molina, Anthem, UnitedHealth Group, and Aetna/CVS) accounted for almost 60% of the pandemic-related increase in MCO enrollment from March 2020 to March 2021 in these states. Earnings reports from Q4 2021 for these five for-profit parent firms (Centene, Molina, Anthem, UnitedHealth Group, and Aetna/CVS) showed year-over-year growth in Medicaid membership (2021 over 2020) ranging from 10 to 20% and for the three firms that provided Medicaid-specific revenue information (Centene, Molina, and UnitedHealth Group) growth in Medicaid revenues ranging from 13 to 43%.

8. Within broad federal and state rules, plans often have discretion in how to ensure access to care for enrollees and how to pay providers.

Plan efforts to recruit and maintain their provider networks can play a crucial role in determining enrollees’ access to care through factors such as travel times, wait times, or choice of provider. Federal rules require that states establish network adequacy standards. States have a great deal of flexibility to define those standards. The 2020 CMS Medicaid managed care final rule removed the requirement that states use time and distance standards to ensure provider network adequacy and instead lets states choose any quantitative standard. KFF conducted a survey of Medicaid managed care plans in 2017 and found that responding plans reported a variety of strategies to address provider network issues, including direct outreach to providers, financial incentives, automatic assignment of members to PCPs, and prompt payment policies. However, despite employing various strategies, plans reported more challenges in recruiting specialty providers than in recruiting primary care providers to their networks. Plans reported that these challenges were more likely due to provider supply shortages than due to low provider participation in Medicaid. In June 2021, CMS announced plans to introduce a series of tools to improve the monitoring and oversight of managed care in Medicaid and CHIP. CMS plans to release reporting templates for required managed care reports (Annual Program Oversight Report, MLR Summary Report, Access Standards Report) as well as technical assistance toolkits (e.g., behavioral health access, strategies for ensuring provider network adequacy) to assist states in complying with various managed care standards and regulations.

To help ensure participation, many states require minimum provider rates in their contracts with MCOs that may be tied to fee-for-service rates. In a 2021 KFF annual survey of Medicaid directors, about two-thirds of responding states with MCO and/or limited benefit contracts (pre-paid health plans, or “PHPs”) reported a minimum fee schedule that sets a reimbursement floor for one or more specified provider types (Figure 10). Additionally, over half of responding states that contract with managed care plans reported a uniform dollar or percentage increase payment requirement in place as of July 2021, most commonly for hospitals. In response to the COVID-19 pandemic, states have options and flexibilities under existing managed care rules to direct/bolster payments to Medicaid providers and to preserve access to care for enrollees. More than one-third of responding MCO states implemented new provider payment and/or pass-through requirements on MCOs in response to the COVID-19 emergency in FY 2021.

9. Over time, the expansion of risk-based managed care in Medicaid has been accompanied by greater attention to measuring quality and outcomes.

States incorporate quality metrics into the ongoing monitoring of their programs, including linking financial incentives like performance bonuses or penalties, capitation withholds, or value-based state-directed payments to quality measures. In a 2021 KFF annual survey of Medicaid directors, over three-quarters of responding MCO states reported using at least one financial incentive to promote quality of care (in a specified performance area) as of July 2021 (Figure 11). Financial incentive performance areas most frequently targeted by MCO states include behavioral health, chronic disease management, and perinatal/birth outcomes. These focus areas are not surprising given the chronic physical health and behavioral health needs of the Medicaid population, as well as the significant share of the nation’s births funded by Medicaid. A number of states reported making changes to their quality incentive programs due to the COVID-19 pandemic, as the pandemic has likely affected clinical practices and timely reporting of quality data. Despite activity in this area, detailed performance information at the plan-level is not frequently made publicly available by state Medicaid agencies, limiting transparency and the ability of Medicaid beneficiaries (and other stakeholders) to assess how plans are performing on key indicators related to access, quality, etc.

As part of managed care plan contract requirements, state Medicaid programs have also been focused on the use of alternative payment models (APMs) to reimburse providers and incentivize quality. Alternative payment models (APMs) replace FFS/volume-driven provider payments and lie along a continuum, ranging from arrangements that involve limited or no provider financial risk (e.g., pay-for-performance (P4P) models) to arrangements that place providers at more financial risk (e.g., shared savings/risk arrangements or global capitation payments). As of July 2021, more than half of responding MCO states identified a specific target in their MCO contracts for the percentage of provider payments or plan members that MCOs must cover via APMs. Of these states, about half reported that their MCO contracts included incentives or penalties for meeting or failing to meet APM targets. For most states, the requirements for APMs were in the 25 – 50% range. States reported setting different percentage requirements depending on the services and population served under the managed care contract. Thirteen states reported that their APM targets were linked to the Health Care Payment Learning & Action Network’s (LAN’s) APM Framework that categorizes APMs in tiers.

While there is some evidence of positive impacts from state use of financial incentives to engage managed care plans around quality and outcomes, the results are more mixed and limited at the provider level. ,,

10. States are looking to Medicaid MCOs to develop strategies to identify and address social determinants of health and to reduce health disparities.

Many states are leveraging MCO contracts to promote strategies to address social determinants of health (SDOH), though how far these efforts will go or how effective they will be remains to be seen. Social determinants of health (SDOH) are the conditions in which people are born, grown, live, work, and age that shape health. In a 2021 KFF survey of Medicaid directors, the vast majority of responding MCO states reported leveraging Medicaid MCO contracts to promote at least one strategy to address social determinants of health in FY 2021 (Figure 12). More than half of responding MCO states reported requiring MCOs to screen enrollees for behavioral health needs, provide referrals to social services, partner with community-based organizations (CBOs), and screen enrollees for social needs. About half of responding MCO states reported requiring or planning to require uniform SDOH questions within MCO screening tools. Fewer states reported requiring MCOs to track the outcomes of referrals to social services or requiring MCO community reinvestment (e.g. tied to plan profit or MLR) compared to other strategies; however, a number of states indicated plans to require these activities in FY 2022.

Communities of color have higher rates of underlying health conditions compared to White people and are more likely to be uninsured or report other health care access barrier. The COVID-19 pandemic exacerbated already existing health disparities for a broad range of populations, but specifically for people of color. We asked states to identify innovative or notable initiatives in this area in our 2021 KFF survey of Medicaid directors. About half of responding states reported managed care requirements and/or initiatives to address health disparities, including Performance Improvement Projects (PIPs), requirements that MCOs achieve the NCQA Distinction in Multicultural Health Care, and pay-for-performance (P4P) initiatives. Finally, given the large number of people covered by Medicaid, including groups disproportionately at risk of contracting COVID-19 as well as many individuals facing access challenges, state Medicaid programs and Medicaid MCOs (which enroll over two-thirds of all Medicaid beneficiaries) can help in COVID-19 vaccination efforts. In response to KFF’s 2021 50-state Medicaid budget survey, states reported a variety of MCO activities aimed at promoting the take-up of COVID-19 vaccinations. States reported MCOs are using member and provider incentives, member outreach and education, provider engagement, assistance with vaccination scheduling and transportation coordination, and partnerships with state and local organizations.

I don’t think the title of your article matches the content lol. Just kidding, mainly because I had some doubts after reading the article.

Your article helped me a lot, is there any more related content? Thanks!