The Medical Loss Ratio (MLR) provision of the Affordable Care Act (ACA) limits the amount of premium income that insurers can keep for administration, marketing, and profits. The ACA requires health insurers to publicly report the portion of their premium dollars spent on health care costs, quality improvement, and other activities in each state they operate in. MLR rebates are based on a 3-year average, meaning that 2021 rebates will be calculated using insurers’ financial data in 2018, 2019, and 2020. Rebates issued in 2021 will go to consumers who were enrolled in rebate-eligible plans in 2020.

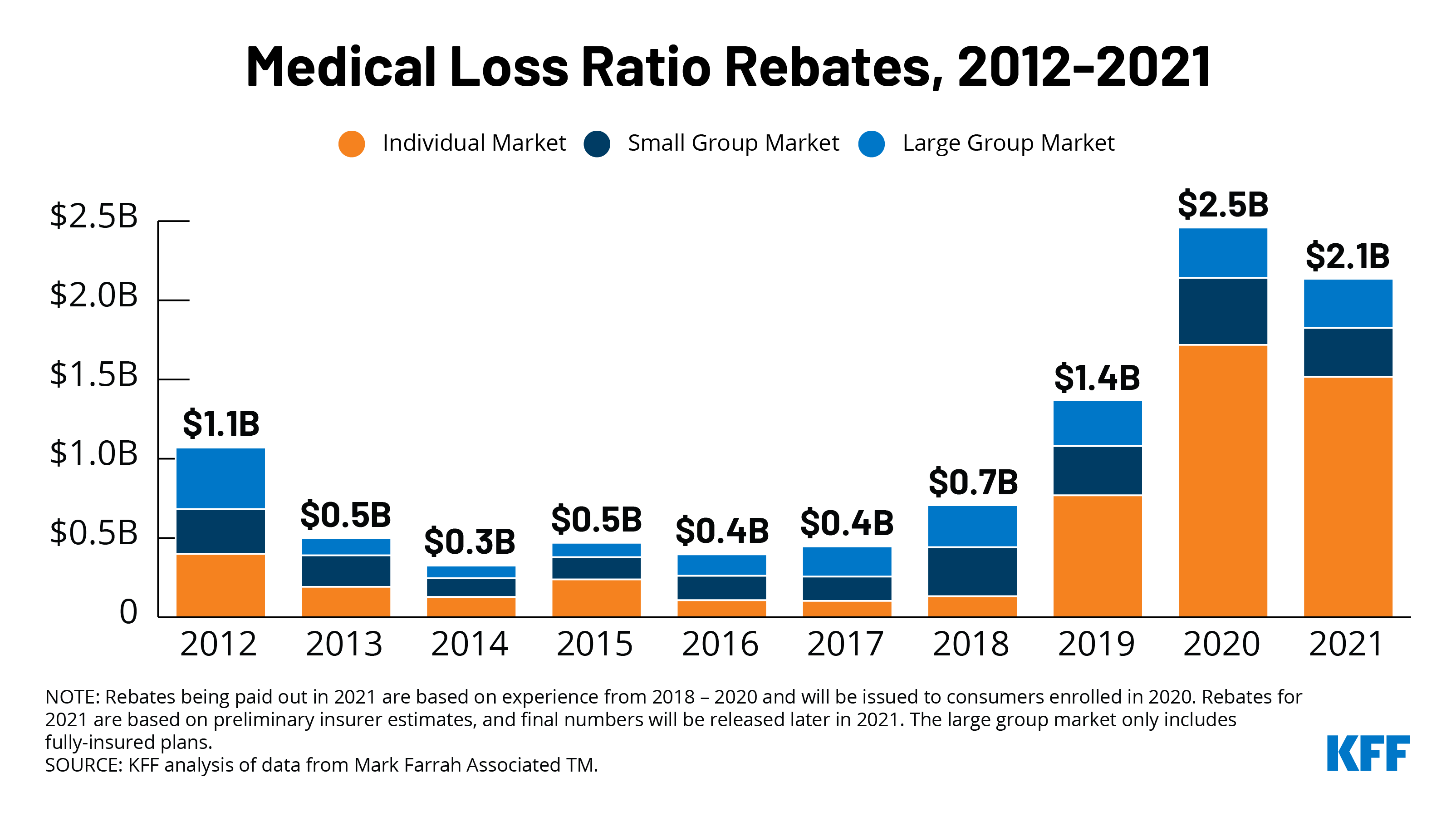

Using preliminary data reported by insurers to state regulators and compiled by Mark Farrah Associates, we find that insurers estimate they will be issuing a total of about $2.1 billion across all markets – the second-largest amount since rebates were first issued in 2012 under the ACA. This year’s rebates are roughly $400 million lower than last year’s record high of $2.5 billion, but more than 50% higher than the amount in 2019 ($1.4 billion, which, at the time, was a record high). These amounts are preliminary estimates, and final rebate data will be available later this year. Some insurers have not yet filed their 2021 rebate estimates.

Expected rebate amounts vary by market, with the majority accounted for by individual market insurers. For 2021, insurers in the individual market estimate they will issue $1.5 billion in rebates, small group market insurers will issue $308 million in rebates, and large group market insurers will issue $310 million in rebates.

| Individual Market | Small Group Market | Large Group Market | Total – All Markets | |

| Total Rebates | $1.52 billion | $308 million | $310 million | $2.14 billion |

| Number of members owed a rebate* | 5,076,000 | 2,429,000 | 3,261,000 | 10,766,000 |

| Average rebate per member | $299 per member | $127 per member | $95 per member | $198 per member |

| NOTES: *The number of members is rounded to the nearest thousand, and shows the average 2020 monthly membership in plans that owe rebates in 2021. These figures do not include health plans managed by the California Department of Managed Health Care. SOURCE: KFF analysis of data from Mark Farrah Associates Health Coverage Portal TM |

||||

These large MLR rebates are likely driven in part by suppressed health care utilization during the COVID-19 pandemic. In the individual market, this year’s rebates are also driven by significant profits in 2018 and 2019 (as rebates issued in 2021 are based on insurer financial performance in 2018, 2019, and 2020). As our previous analyses have shown, individual market insurers were highly profitable in 2018 and 2019 despite the repeal of the individual mandate and successive years of decreases in average premiums.

In 2020, there were several factors driving health spending and utilization down. Hospitals and providers cancelled elective care early in the pandemic and during spikes in COVID-19 cases in order to free up hospital capacity, preserve supplies, and mitigate the spread of the virus. Many consumers also chose to forego routine care in 2020 due to social distancing requirements or similar concerns. Telehealth claims increased and insurers still had to foot the bill for COVID-19 testing and treatment costs, but these expenses did not offset the decreases in in-person care. An analysis on the Peterson-KFF Health System Tracker found that health spending fell slightly last year, making 2020 the first year on record to see a drop in health spending in the U.S.

Because of these dynamics, by mid-2020, many insurers were left with higher levels of premium profits than they were anticipating when they set their 2020 premiums well before the pandemic emerged. In response, a number of insurers waived certain out-of-pocket costs for telehealth visits and COVID-related services or even offered premium holidays at some point in 2020, which had a downward effect on rebates. Insurers that waived some patient costs or offered premium holidays will owe less in rebates than they otherwise would if they had not taken these steps to increase their claims costs or lower their premium revenue. Our earlier analysis published on the Peterson-KFF Health System Tracker found that almost 90% of enrollees in the individual and fully-insured group markets were in a plan that waived cost-sharing for COVID-19 treatment at some point during the pandemic. The analysis also found that 4 in 10 enrollees in these markets were also in plans that offered some form of premium credit or reduction in 2020. Some insurers might have taken these steps in the absence of the ACA’s loss ratio requirements (perhaps to preempt a federal mandate to cover COVID-19 treatment), but it is unlikely premium holidays and cost waivers would have been so common if the MLR provision wasn’t in effect. Additionally, claims costs for COVID-19 treatment began to rise toward the end of the year during the November and December surge, which also had a downward effect on rebates.

On average, insurer medical loss ratios in the individual market were 74% in 2020, without accounting for quality improvement expenses or taxes. In the small and large group markets, 2020 average loss ratios were 79% and 86%, respectively. (These are simple loss ratios, calculated as the share of premium income paid out as claims, so they do not align perfectly with the ACA MLR thresholds). The MLR provision requires that insurers in the individual market and small group market spend at least 80% of their premium income on health care claims and quality improvement, leaving the remaining 20% for administration, marketing expenses, and profit. The MLR threshold is higher for large group insurers, which must spend at least 85% of their premium income on health care claims and quality improvement (only fully-insured large group plans are subject to the MLR rule; 67% of covered workers are in self-funded plans to which the MLR threshold does not apply). Insurers that fail to meet the applicable MLR threshold for their market are required to pay back excess profits in the form of rebates to their enrollees.

Insurers in the individual market may either issue rebates in the form of a premium credit or a check payment and, in the case of people with employer coverage, the rebate may be shared between the employer and the employee. If the amount of the rebate is exceptionally small ($5 for individual rebates and $20 for group rebates), insurers are not required to process the rebate, as it may not warrant the administrative burden required to do so.

Rebates in the small and large group markets are similar to the amounts in recent years. In the case of employer-sponsored insurance plans, the cost of coverage is often split between the employer and employees. Therefore, for many employer-sponsored plans, the handling of refunds to employers and employees may depend on the plan’s contract and the way in which the policyholder and participants share premium costs.

Looking ahead to rebates and premiums in 2022, insurers have the difficult task of predicting the continued impact of the pandemic. Insurers setting premiums for the 2022 plan year need to factor in several pandemic-related considerations, including but not limited to: potential pent-up demand for care, the negative impact of foregone care on the health of some enrollees, and the take-up of COVID-19 vaccinations and whether they need to be re-administered next year. Moreover, the Biden Administration and Congress have made several regulatory changes that will affect enrollment and costs in the Marketplaces for at least the next two years. Biden has opened a Special Enrollment Period (SEP) allowing anyone to sign up for Marketplace coverage until September. The American Rescue Plan Act of 2021 also temporarily expanded eligibility for Marketplace subsidies and increased the financial assistance to those who already qualified for subsidies. The Congressional Budget Office expects that these changes will drive more than a million additional enrollees into the individual market over the next two years, but the extent of enrollment growth and whether these new enrollees will be more or less expensive on average than current enrollees remains to be seen.

| We analyzed insurer-reported financial data from Health Coverage Portal TM, a market database maintained by Mark Farrah Associates, which includes information from the National Association of Insurance Commissioners. The dataset analyzed in this report does not include NAIC plans licensed as life insurance or California HMOs regulated by California’s Department of Managed Health Care. All individual market figures in this issue brief are for the individual health insurance market as a whole, which includes major medical insurance plans and mini-med plans sold both on and off exchange.

Total rebates are based on preliminary estimates from insurers. Since 2014, the total rebate amount issued across the individual, small group and large group markets has varied by 3 to 5% from insurer estimates. In some years, final rebates are higher than expected and in other years, final rebates are lower. |